Drewry Maritime Financial Research (DMFR), the investment research arm of global shipping consultancy Drewry, remains bullish about continued high stock prices and rising profitability in the booming container carrier sector. In an analysis in the December edition of Drewry’s Container Forecaster, DMFR analyses factors supporting its conclusion that equity investors should ‘stay put’ in the sector and that annual carrier industry profits will rise again in 2022.

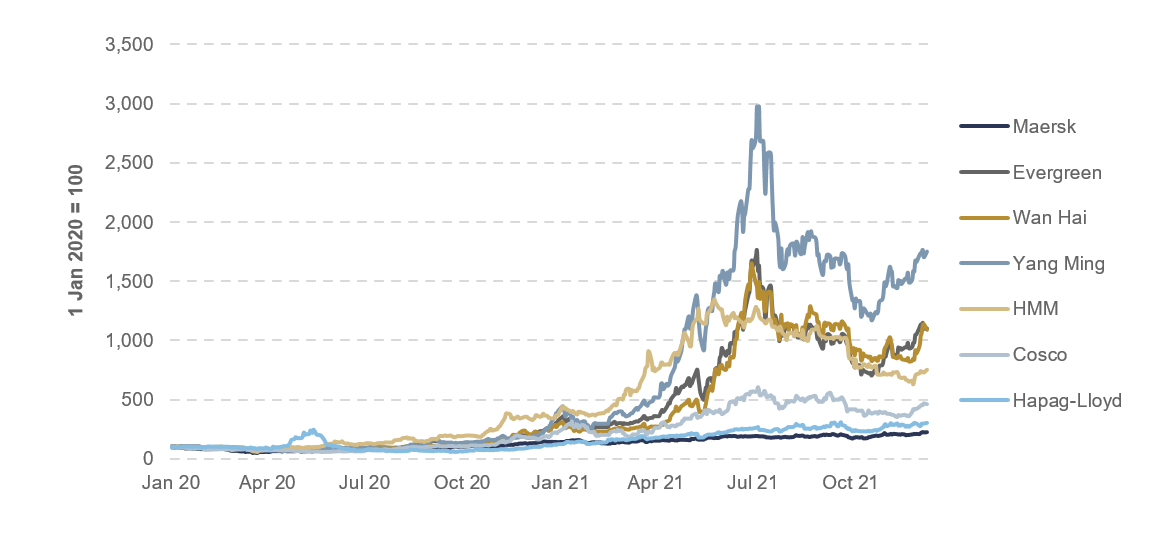

The strong performance in the global container shipping sector has generated very handsome spill-over benefits for stock investors (see Figure 1). The returns since the start of 2020 have been astronomical.

Asian liner operators were the top performers; with Yang Ming up by 1,583% (as of mid-December 2021), followed by Evergreen Marine’s gain of 987% and Wan Hai’s 976%. HMM generated returns of 621%. More modest growth was seen in Europe, where Hapag-Lloyd shares increased by 192% and Maersk’s by 123%.

Part of this remarkable performance can be attributed to strengthening balance sheets as data from 12 carriers suggests cumulative debt has reduced by $3.5 billion between end-December 2020 and end-September 2021 to $73.2bn. Quite a number of carriers are in a net cash position, meaning their cash balance exceeds total debt, a rarity for the sector.

Clearly, the pandemic and ensuing supply chain crisis that supercharged carrier profits has been the primary driver for the share price bonanza. This was reinforced when share prices bounced back in November after discovery of the Omicron variant, having previously been in retreat since July when there was greater hope for swifter market normalisation.

To further boost investors’ confidence, major shipping lines are also buying back shares. Maersk’s directors have approved an additional share buyback programme of DKK 32 billion ($5bn) over the years 2024 and 2025, bringing the total of outstanding share buyback programmes to DKK 64bn ($10bn) from 2022 to 2025. Cosco, too, announced on 6 December that the board proposed a share repurchase mandate up to 10% of its A- and H shares in issue, pending shareholder approval.

Source: DMFR, Yahoo finance, Share prices as of 15 December 2021

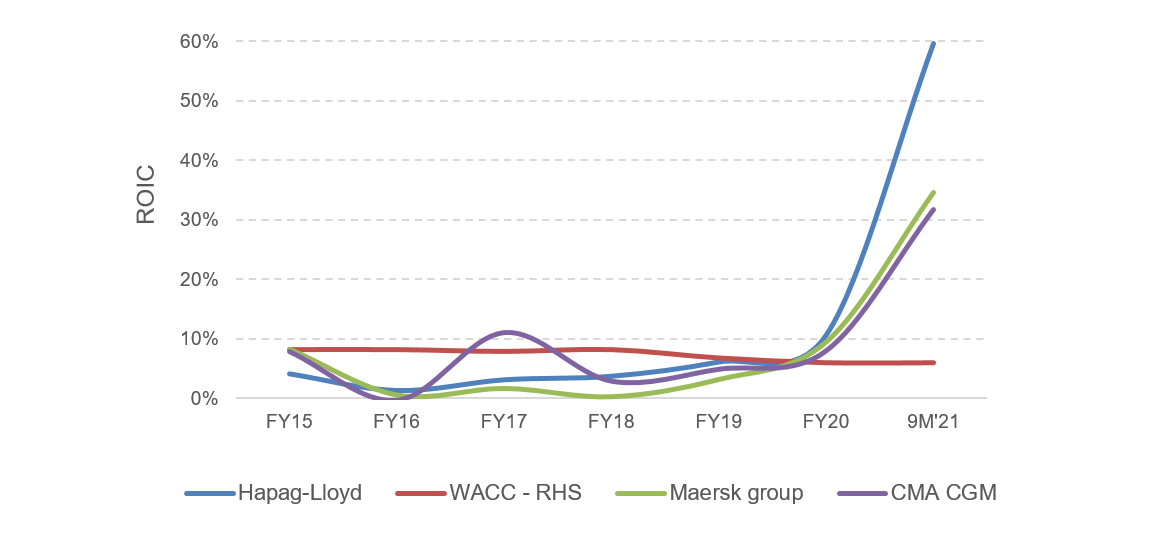

Source: Company, DMFR; note – WACC numbers are as reported by Hapag-Lloyd. We have considered it as a proxy for container shipping WACC because Hapag-Lloyd is a pure play container shipping company

Is it time to exit container shipping stocks?

Given strong stock performances, and the assumption that spot sea freight rates have peaked, some investors may be tempted to exit the container shipping space. However, we see three key reasons to stay positive about the sector:

- The new Covid variant, Omicron, has increased the risk of extended supply chain disruption, which could prop up spot rates for longer and assist contract negotiations;

- Strong free cash flow in the next two years should lift share prices. Maersk has estimated that the group is expecting FCF of about $14.5 billion by end of 2021. Based on that, we can safely presume that the industry will report a free cash flow in excess of $100bn for full year 2021 after reporting $68bn in 9m21 (cumulative of 11 carriers). This should ensure further share price appreciation as cash is paid to shareholders in the form of dividends and new investments are made;

- Returns on invested capital to be above the weighted average cost of capital (WACC) for a more sustained period. We think the current congestion is an opportunity for shipping companies to obtain better (and longer) contract terms from shippers, who will want to ensure their cargo can be moved and avoid high volatility in prices. This will mean sustained profits and higher returns on invested capital versus WACC.

Our view

Given the current scenario of supply chain logjams and rising threat of the Omicron virus, Drewry is once again upgrading its annual forecast for 2021 from our previous guidance of $150bn to $190bn, at a margin of approximately 43%. The smoother earnings forecast rationale stems from a pivot away from the volatile (and likely retreating) spot market towards longer-term contracts that are expected to be signed at significantly higher levels in upcoming negotiations. This will ensure high profits for the global container shipping sector that will continue to generate very handsome spill-over benefits for stock investors through both soaring share prices and generous dividends.

Source : Hellenic Shipping News