The tension in the relationship between Australia and China, already evident since the start of the pandemic, hasn’t abated until now. On the contrary, it seems to be worsening, which in turn, is causing an upset to regular dry bulk trade patters. In its latest weekly report, shipbroker Intermodal commented that “the unfolding last week of a trilateral defence pact between the United States, Australia, the United Kingdom (AUKUS) envisages a wide range of collaboration, but at its core is an agreement to start consultations to help Australia acquire a fleet of nuclear-propelled submarines. Believe AUKUS is an interesting development in the context of the already intensified geopolitical tensions between Australia and China, which have already led to a shift in trading patterns, particularly as far as dry bulk trade is concerned.

Source: Intermodal

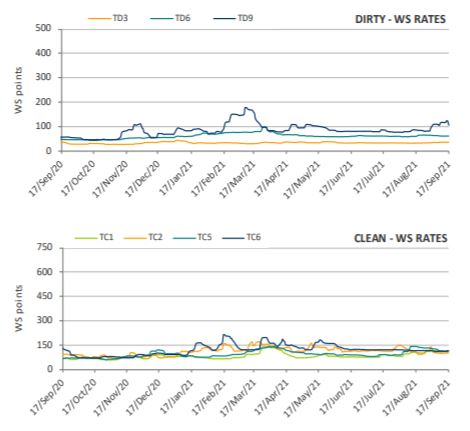

According to Intermodal’s Mr. Christopher Whitty, Director of Towage and Marine Port Services, “in particular, China’s ban on Australian coal since Q42020 has triggered inefficiencies in coal trading, with wide price arbitrages developing between China and the rest of the world for both metallurgical coal used by the steel industry and thermal coal used in power generation. The supply tightness has been more severe on metallurgical coal, the price of which has surged to record high levels, with China scrambling for supplies simulateneously with the rest of the world, steel production of which continues to grow. Australia is the world’s largest met coal exporter (approx. 59.0% of global seaborne met coal exports) and 2nd thermal coal exporter (approx. 22.0% of global seaborne thermal coal exports). China’s coking coal imports from Australia have come down to zero YTD 2021 vs a more than 50% share in imports during the previous two years. Imports from Mongolia so far have failed to meet increased demand amid COVID related supply disruptions and China had to increase its met coal imports share from Russia and the West (particularly the US and Canada), the last traditionally being primariy origins of imports for Europe. On the other hand, Australia coking coal is absorbed by steel mills outside China, as global steel production excl. the latter is up 16.0+% y-o-y (YTD Jan-Jul) and Australia coking coal has turned out cheaper than US coking coal despite the overall price surge. This trade shift has increased ton-miles and dry bulk fleet inefficiencies supporting Atlantic freight rates higher for longer”.

Whitty added that “in the meantime, China’s policy pledge for emissions cuts seems to be further supporting ton-miles for dry bulk, despite the country’s crude steel production declining y-o-y over the past two months and iron ore price collapsing below $100/ton recently from $230/ton in mid-July. We believe that in the short term, the severe coking coal and coke shortage in China as a result of the above policies is forcing crude steel production to adjust downwards earlier, but is incentivizing purchases of cheaper iron ore particularly from the Atlantic”.

“Till recently, demand for cargoes of crucial raw materials like iron ore and coal have overall jumped this year, outpacing active fleet growth, particularly if congestion is factored in, as economies recover from the pandemic. As new market dynamics develop and shape a new post pandemic landscape, we want to believe that these will become new fundamentals that can continue to propel ultimately demand for seaborne transportation of dry bulk commodities in the long run”, Intermodal’s analyst concluded.

Source : Hellenic Shipping News

Join our WhatsApp channel for more updates:

Join our WhatsApp channel for more updates: Subscribe to our YouTube channel for more updates:

Subscribe to our YouTube channel for more updates:

{kind=link}